How Small Business Deductions Can Help Reduce Your Tax Bill

Most businesses start small and grow over time. The Canada Revenue Agency (CRA) knows that small businesses often bear higher expenses, particularly at their inception. To help these small businesses grow and to encourage entrepreneurship in the country, the agency introduced the Small Business Deduction (SBD) to lower taxes payable while businesses are working to establish themselves.

What is Small Business Deduction?

Corporations in Canada pay a basic federal tax rate of 38%. The CRA offers a federal tax abatement of 10% that can reduce the corporate tax rate to 28%. If a company qualifies for the SBD, the CRA reduces the tax rate by another 19%, so the payable tax rate will be just 9% on the first $500,000 of business income in a tax year.

What is “business income”?

According to the CRA, business income is defined as the total monetary value that your business receives for the products and services it provides. This value generally includes revenues earned in Canada and internationally. However, for the purposes of the SBD, you can only include the business income earned from operations carried out within Canada.

The CRA introduced the SBD to reduce the tax rate a corporation pays on its business income. To qualify for the SBD, a business:

- should be a private corporation,

- should be a Canada-based organization, and

- its taxable capital employed in Canada should not exceed $10 million.

For a Canadian-controlled private corporation (CCPC), the SBD applies to the lesser of the following:

- business income limit of $500,000,

- an organization’s taxable income for the year, or

- the annual business income from business operations carried out in Canada.

How Can the Small Business Deduction Reduce Your Tax Bill?

Let us understand these calculations with the help of an example. John is a real estate agent who lives in Toronto. He lost his job due to the pandemic and started a small baking business from his home. His business earns $200,000 annually. Taxed at a rate of 28%, his tax bill would total $56,000 (28% of $200,000). If John applies the SBD, his tax bill will reduce to $18,000 (9% of $200,000).

Mary is a famous fashion designer and has a large boutique. Her business earns $600,000 per year, and her tax bill amounts to $168,000 (28% of $600,000). If Mary applies the SBD on the first $500,000 of her business income, her tax bill will amount to $73,000, which is the sum of $45,000 (9% of $500,000) and $28,000 (28% of $100,000).

Both the above examples show how incorporating a small business can significantly help to reduce your tax bill. Incorporating a business requires an initial investment of time, but eventually, it can bring about major tax savings.

The Ontario government also offers the SBD for provincial tax rates. If your business is eligible for the SBD, you can calculate your tax bill using the lower tax rate. For instance, in Ontario, the higher rate is 11.5%, and the lower rate is 3.2%. A corporation can apply the lower tax rate on the income that would also be eligible for the federal SBD.

You should note that the SBD applies to the income of the primary CCPC’s associated businesses as well. For example, if you have an e-commerce store, and you opened an associate company for warehousing inventory, the SBD would apply to the combined income of both companies.

How Can The CRA Take Away Your SBD?

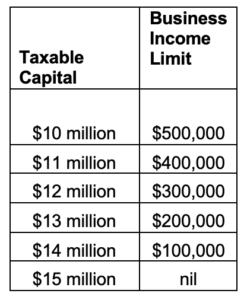

The CRA begins to reduce the SBD if a CCPC’s taxable capital in Canada surpasses $10 million. For every $1 million increase in a CCPC’s capital, the business income limit reduces by $100,000 and becomes zero once the capital reaches $15 million. The below table shows how the business income limit will reduce as capital increases:

Starting January 2019, the CRA introduced another method to phase out the SBD. This method also applies to a CCPC with taxable capital in excess of $10 million. Under this rule, its business income limit of $500,000 starts phasing out if a corporation earns more than $50,000 in passive investment income.

Continuing with the above example of the e-commerce firm, let’s say the company rented a portion of its warehouse to another firm. The active business income would be the profit earned from the e-commerce platform. The rental money will be considered the company’s passive investment income, as its core activity is e-commerce sales.

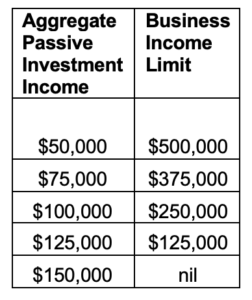

For every $25,000 increase in passive investment income, the business income limit that will be eligible for the SBD will reduce by $125,000. Once the passive investment income reaches $150,000 annually, the CCPC can no longer claim the SBD. The below table shows how the business income limit will reduce as passive investment income increases:

Consult With a Financial Professional at Edelkoort Smethurst CPAs LLP for More Information

If you are a small business owner or a self-employed individual and wish to learn more about how to maximize tax benefits for your business, please contact the Chartered Professional Accountants at Edelkoort Smethurst CPAs LLP at 905-517-2297 or by contacting us online.