The Fraud Triangle: How an Auditor Can Help Mitigate Threats

The pandemic has created a tenuous situation for many employers and employees. With erratic business closures imposed, as well as frequent lockdowns, running a business has been a fraught exercise for many, and employment has become less secure as a result. For those who are still working, they may be facing reduced hours or increased job insecurity, which in turn can create panic about maintaining their ongoing expenses.

The question employers need to consider, is do these employees pose a risk to your business? The unfortunate fact is, the temptation to gain a financial advantage is likely at an all-time high among many employees, increasing the risk for fraudulent activity. Fraud refers to intentional deception used for personal gain. While fraud can happen in any number of circumstances, employee fraud is frequent, and employers need to be aware of the warning signs, as well as how they can mitigate the risks of their own employees engaging in this activity.

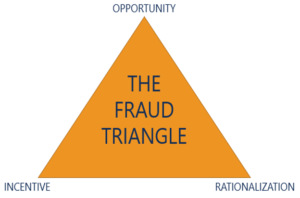

What is the “Fraud Triangle”?

The fraud triangle is a framework commonly used in auditing to identify potential fraud, or an increased likelihood, so employers can implement tools to discourage fraud. The fraud triangle outlines three elements that contribute to increasing the risk of fraud:

- Incentive

- Opportunity

- Rationalization

Incentive

Tough economic conditions for employees may lead ordinarily excellent employees to make decisions they never would under better circumstances. These employees may have become overwhelmed by the economic situation, leading them to wonder if they could “borrow” money from their employer to tide them over, with the intention of repaying the funds before they’re noticed. This could include taking cash, or company inventory and selling it on their own.

Other incentive situations relate to potential bonus opportunities. Employees may generate false transactions that increase their chances of receiving a bonus. These transactions could include sales to non-existent customers, or inflating the numbers of existing transactions. This activity often requires the efforts of more than one employee to pull off successfully, due to the internal controls many businesses have in place. However, if your accounting policies are not well defined, it may be simpler for a single employee to create false reports and have them go unnoticed, at least for some amount of time.

Opportunity

Fraud is more likely to happen if employees perceive that it can be easily done. If your organization’s internal controls are perceived as weak or easily manipulated, this may encourage employees to consider taking action that will benefit them and hurt your business. This is amplified if the employees see (or perceive) other employees or management taking advantage of the internal systems for their own benefit.

Rationalization

How and under what conditions will otherwise great employees rationalize the decision to commit fraud? Employees who feel that their employer has “done them wrong” could be motivated to steal from the company. Examples of issues that could lead to this feeling, especially during these challenging times, may include:

- Reduced hours of work (full-time to part-time)

- Reduced wages or salary

- Reduction of benefits

- Temporary layoffs with unpredictable timing

As mentioned above, if employees believe that management is taking advantage of company situations to their benefit, especially while employees are facing a reduction in work or pay, they may be more likely to rationalize fraud. Some employees may simply feel backed into a corner, and as though there is no other solution. This is most likely to occur with employees who face consequences like losing their job due to business reduction, or losing their house because they can’t make mortgage payments.

How an Experienced Auditor Can Help Lower the Risk of Internal Fraud

An experienced auditor will review a business’s financial statements, internal controls and other factors that can contribute to or help identify instances of fraud. In addition to pointing out potential fraud, an auditor will also advise a business on how to improve their internal systems to prevent fraud from occurring in the first place.

Here are just some of the steps an employer can take to reduce their risk of employee fraud:

- Ensure that your internal controls are working effectively.

- Make sure that your accounting policies are well defined.

- Review issues such as abnormal inventory losses on a regular basis.

- When fraud is a concern, employ a forensic accountant. Forensic accountants apply a range of skills and methods to determine whether there has been financial reporting misconduct that may not otherwise be found.

- Set an example. As a business owner, it’s important not to appear to be thriving, while employees suffer, or appear to be taking advantage of a situation for your own benefit.

Contact Edelkoort Smethurst CPAs LLP for Assurance and Auditing Services

Edelkoort Smethurst CPAs LLP in Burlington can provide your business with complete assurance and audit services to ensure your company’s full compliance with tax regulations and keep tabs on the financial health of the business. Our CPAs are highly skilled and serve the local Burlington and Halton business community with professionalism and a dedication to excellent service. To speak with one of our knowledgeable Chartered Professional Accountants, please contact us online or by telephone at 905-517-2297.