Canada Emergency Wage Subsidy: An Update

We previously wrote a blog about the Canada Emergency Wage Subsidy (CEWS) program back in April. Recently, the federal government provided proposed updates to the program after consulting with several employers and businesses across the country on how the program could have the most impact.

An Overview of the Original CEWS Program

The backgrounder document provided by the Department of Finance sets out a summary of the original CEWS program as follows:

The CEWS was put in place for an initial 12-week period from March 15 to June 6, 2020, providing a 75-per-cent wage subsidy to eligible employers. On May 15, 2020, Finance Minister Bill Morneau announced that the Government of Canada would extend the CEWS by an additional 12 weeks to August 29, 2020. This announcement was part of a public consultation the government undertook to ensure the CEWS was best positioned to help get Canadians hired back quickly as provincial and territorial economies begin to reopen. The government announced on June 10, 2020, that the same eligibility criteria for the initial three 4-week periods (March 15 to June 6, 2020) would continue to apply for Period 4 (June 7 to July 4, 2020).

The government proposed a further extension of the CEWS, until December 19, 2020, providing proposed program details until November 21, 2020, and has shared a draft of the legislative proposals. These proposals would adapt the CEWS to support more workers and businesses, better protect jobs and promote growth, and effectively respond as the economy continues to reopen. The draft legislative proposals would also give the government some flexibility to ensure the wage subsidy can adjust to the needs of businesses if economic conditions change. The estimated total fiscal cost in 2020-21 for the CEWS program that is being announced today is $83.6 billion.

To ensure the program is having the intended effect of maximizing the ability of Canadian businesses to retain staff during the hardships faced as a result of the pandemic, the government consulted with a variety of employers across the country. Several key points were identified as a result of these consultations:

Cliff Effect

Employers did not like the effect of the elimination of the 30% revenue drop and favoured a gradual reduction in the CEWS rate as revenues increase. There was a concern that businesses would be abruptly cut off from CEWS before they were ready once their revenue drop became less than 30%.

Revenue Test

Other employers stated that the 30% revenue decline test was too stringent. What happens to businesses that peak with a 20% to 25% drop and there is a slow recovery in demand for these products or services as the economy recovers? Quoting one of the responders, “Having options of a tiered support may better support those organizations that are still hit really hard by the pandemic but that have not seen a full 30% reduction in revenue. At the moment it is all or nothing, you either get 0-10% support or 75% support but have nothing for those in between.”

Extension

Another point raised was how long can the support go on. Some businesses may recover by August 29 but not all.

Highly Impacted Firms

Just as some businesses may take longer to recover, some firms are more impacted than others. Depending on the service or industry, the impact of the pandemic is likely to affect businesses differently.

Changes to the CEWS Program

Effective July 5, 2020, the CEWS would consist of two parts:

- a base subsidy available to all eligible employers that are experiencing a decline in revenues, with the subsidy amount varying depending on the scale of revenue decline.

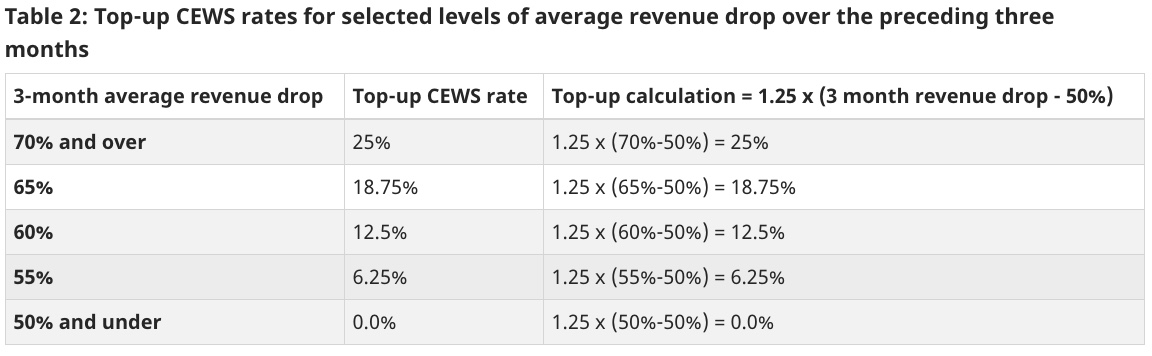

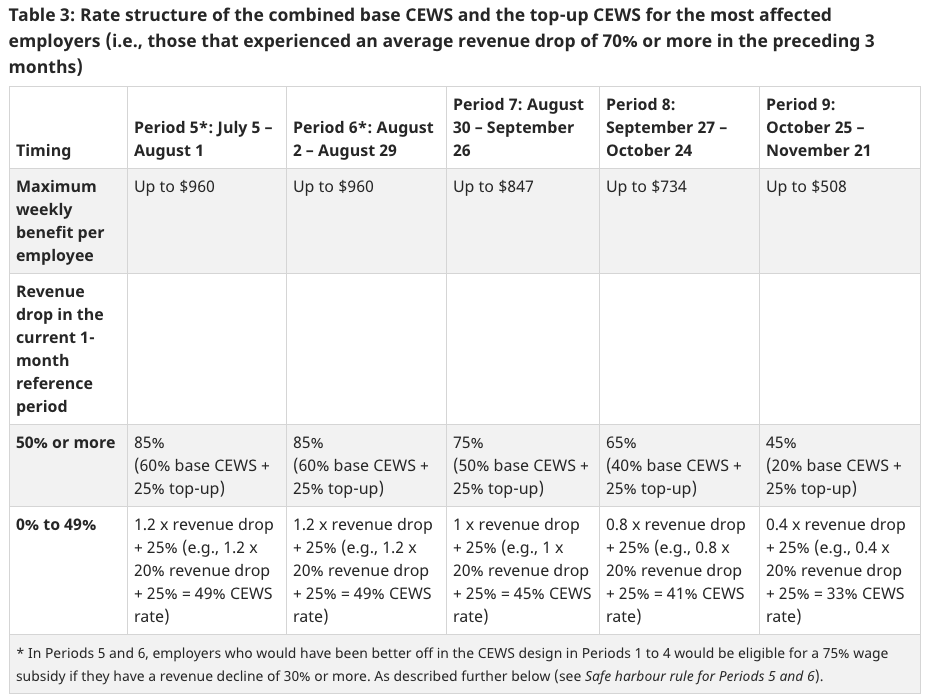

- a top-up subsidy of up to an additional 25 percent for those employers that have been most adversely affected by the COVID-19 crisis.

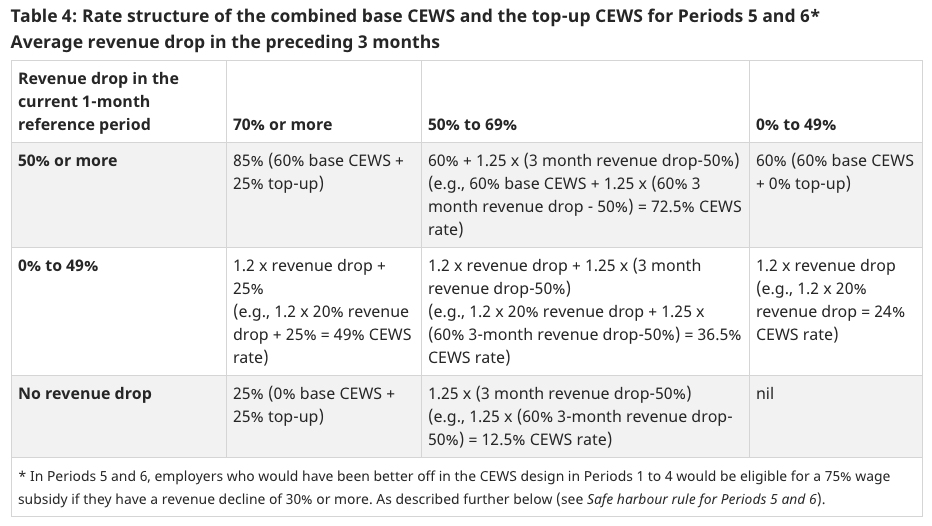

The two-part rate would be set up for active employees. For furloughed employees, there will be a separate CEWS rate structure. As well, there is a “safe harbour” condition to ensure that employers would have access to a CEWS rate to August 29th at least as favourable as the initial CEWS rates.

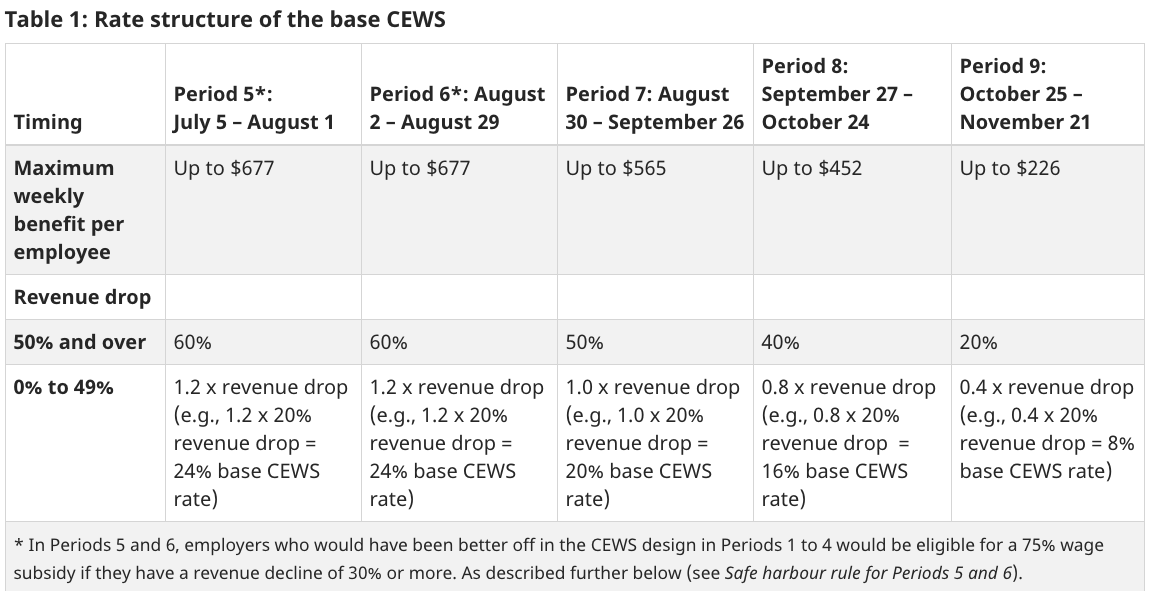

The base CEWS amount for active employees will be based on a specified rate, applied to the amount of remuneration paid to the employee for the eligibility period, on the remuneration of up to $1,129 per week. The rate of the base CEWS will vary depending on the level of revenue decline.

Effective July 5, 2020 (i.e., Period 5 and subsequent periods – see Table 1 below), employers that have been affected by the COVID-19 crisis would be eligible for a base CEWS amount for active employees. This base CEWS would be a specified rate, applied to the amount of remuneration paid to the employee for the eligibility period, on remuneration of up to $1,129 per week. The rate of the base CEWS would now vary depending on the level of revenue decline, and its application would be extended to employers with a revenue decline of less than 30% (see Table 1). This expansion would mean that all eligible employers with a revenue decline would now qualify for CEWS support.

The maximum base CEWS rate would be provided to employers with a revenue drop of 50 percent or more. Employers with a revenue drop of less than 50 percent would be eligible for a lower base CEWS rate mentioned at the end of the last paragraph. This allows for a gradual reduction in CEWS as a business’ revenue increases. Similarly, the maximum rate will be a drop from 60% in periods 5 and 6 (July 5th to August 29th) to 20% in period 9 (October 25 to November 21).

The charts below provide very detailed information on the changes. The charts are complex and so the CRA has generated a new, enhanced online CEWS calculator and Excel spreadsheet as of August 11th. The online calculator is best suited for smaller employers and large employers may find the spreadsheets more useful, especially if they can import the required data from their files.

The overall CEWS rate would be equal to the top-up CEWS rate plus the base CEWS rate. Table 3 shows the combined base and top-up CEWS rates for Periods 5 to 9 for the most adversely affected employers.

Employers Should Seek the Assistance of Experienced Financial Professionals for Assistance

The new program involves several qualifying factors and will be applied incrementally depending on need. It has become much more complex than the initial offering, and many employers may find themselves wondering about their entitlements. For assistance, we recommend contacting an experienced professional accountant to ensure your company maximizes the benefit you are entitled to under the revised CEWS program.

If you wish to become more familiar with the new legislation or have questions about your business’s eligibility or need assistance with applying for this subsidy, please contact the Chartered Professional Accountants at Edelkoort Smethurst CPAs LLP by calling 905-517-2297 or by contacting us online.